Welcome to day 2 of patent data week!

As I wrote yesterday, towards the end of February, I started working on what was supposed to be a single post about using patents to measure innovation (analogous to this post on whether academic citations are a good measure of the impact of new ideas). It turned into four posts I’m posting to substack and the podcast over the week:

Tuesday: Patents (weakly) predict innovation

Wednesday: Do studies based on patents get different results?

If you can’t bear to wait though, all the posts are up on New Things Under the Sun (.com): just click the links above.

And now, on to the second of this four-part series…

Patents (Weakly) Predict Innovation

This article will be updated as the state of the academic literature evolves; you can read the latest version here. You can listen to this post above, or via most podcast apps here.

Lots of social science research about innovation relies on patents as a way to measure innovation. Is that a bad idea? One way to validate the use of patents as a measure of innovation is to see how well patents are correlated with other measures of technological progress. There is a lot of work on this, and it typically finds a small but positive relationship.

New Products

Let’s begin with Argente et al. (2023) who study the introduction of new consumer products, mostly sold in grocery stores and drug stores, which they measure by the introduction of new UPC codes. As discussed in more detail here, they also have data on the number of patents firms have in related product categories. Across all firms, they find that firms that seek a patent in a given product area are also more likely to introduce new UPC codes in the same category. For example, they find that if a firm’s patents in the previous year increases by 10%, the number of new products released increases by about 0.4%. A small effect, but pretty precisely estimated given they have so much data.

Igami and Subrahmanyam (2019) focus on a more innovative industry than consumer goods: the semiconductor industry. They have data on all 178 active firms in the sector between 1976 and 1998 and a very simple measure of innovation: did the information storage capacity of the firm’s frontier products increase over the preceding year? An improvement happens for roughly 35% of observations (where each observation is a firm in a given year). That means if you simply assume there are never any improvements, you’ll be correct 65% of the time. They then ask whether knowing the number of patents the firm applies for in the preceding year can help you beat this benchmark.

They find, yes, it helps a tiny bit, because when a firm seeks more patents it’s a bit more likely to improve its products. Without patents, you can guess correctly 65% of the time by always guessing “no improvement.” In a model where you are more likely to guess there has been an improvement when you see more patents in the preceding year, you can increase the share correct to about 67%. If you restrict your count to patents assigned to the most relevant technology categories for semiconductors, you can push the share of the time you correctly guess if there was an improvement or not to about 70%.

Broader Measures of Technological Progress

Benson and Magee (2015) broaden the inquiry to a sample of 28 different technologies. For each of these technologies, they estimate the rate of technological improvement based on metrics appropriate to the technology. For example, for LED technology they look at improvements in lumen-hours per dollar. For progress in PV solar panel technology, they look at kilowatt-hours per dollar. To measure progress in aircraft transport, they look at passengers multiplied by miles-per-hour. For each of these metrics, they convert the gains into a percent improvement rate over some unit of time. Among their 28 technologies, there’s been the fastest rate of improvement for optical information transmission technologies and wireless information transmission technology, and the slowest rate of improvement for electric motors and milling machines.

They then identify patents related to these 28 different technologies, using the technology classifications assigned to patents and compare improvement rates to various patent-related metrics. Below, I compare rates of progress to two different patent-based metrics. On the left, we’ve got the rate of improvement relative to the total number of related patents over 1976-2013 (on a log scale). On the right, we’ve got the rate of improvement relative to the total number of patents, weighted by citations received within the first three years (citations are common way to assess the value of patents).

There is a positive correlation between patents and these various measures of innovation, and this correlation is a bit tightened when we try to adjust for the quality of patents. But it’s a pretty noisy correlation.

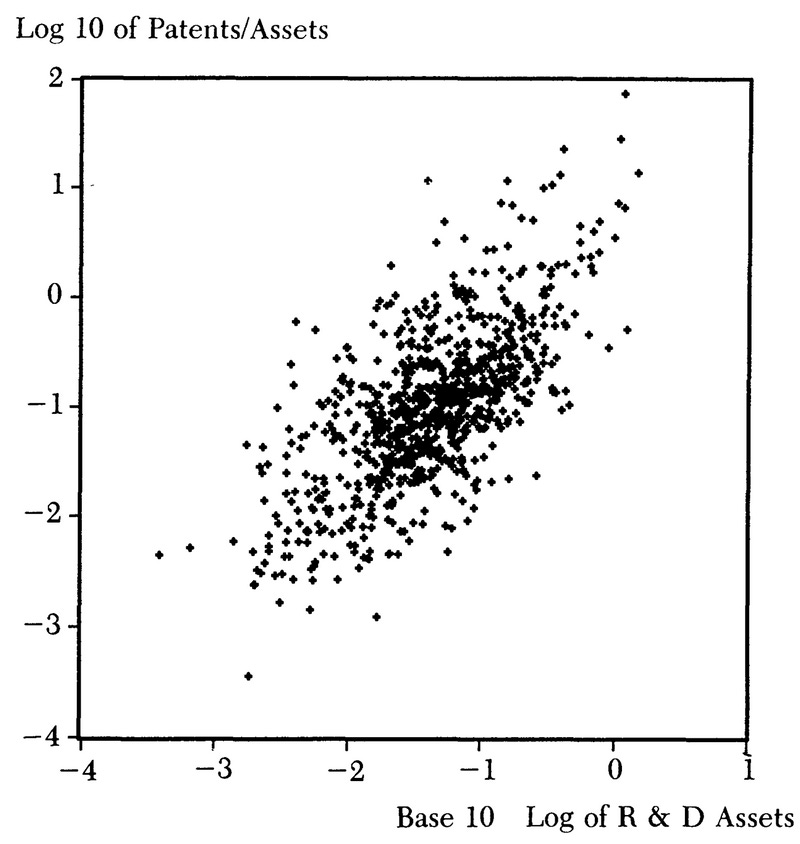

Patenting and R&D

Let’s look at one more fairly direct measure - spending on R&D - before we turn to a more complex measure. Firms will certainly vary in how effective they are at converting R&D spending into innovation, but all else equal, firms that spend more on R&D probably get more innovation than those that don’t. Are patents correlated with R&D spending?

Again, yes. The following figure is taken from Griliches (1990), a classic survey of the patent literature. The plot compares R&D to patenting, but controlling for the size of firms by dividing each by the size of the firm’s assets. More patents per asset, more R&D per asset.

Across firms, this correlation is very tight, but even if we follow a single firm over time, the years when it does more R&D will also tend to be years it obtains more patents (see Griliches 1990).

Productivity and Patents

Finally, we can look at the link between patenting and total factor productivity (hereafter TFP) growth, which is often used as a proxy for technological progress. The basic idea behind TFP is that if you can squeeze more economic outputs out of the same number of inputs (for example, capital and labor), then that’s a reflection of better technology. The challenge is you can’t measure TFP directly; instead, you directly measure outputs (often just total sales) and inputs and try to predict the outputs with the inputs. Something like the gap in your predictions is your measure of technology. It’s a nice concept because it’s a general purpose measure of technology, but it’s very noisy and can be affected by things other than technological progress.

The evidence that raw patent counts positively predict TFP growth is pretty weak. Kalyani (2023) looks at the link between patenting and TFP growth for manufacturing firms in the USA, restricting analysis to firms filing at least 10 patents between 1991 and 2014. For each firm, for each year, he calculates the growth in TFP over 5 years, and then compares that to patenting. Within a given industry, in a given year, he finds that a firm with 10% more patents tends to experience about 0.5% higher TFP growth. But this effect is not statistically significant and actually turns negative (though again, not statistically significant) under some specifications.

Kalyani (2023) and Park and Park (2006) perform a similar exercise at the industry level, linking the growth of TFP in various manufacturing industries to the number of new patents in that industry. When Park and Park adjust for average TFP growth rates in a given year and for a given industry, they find a 10% increase in patents is associated with a 1.6% increase in the industry’s TFP growth. Kalyani (2023) finds a 10% increase in patenting is associated with a 1.4% increase in TFP growth. Neither result can be confidentially distinguished from zero though.

Finally, Porter and Stern (2000) looks at the link between patenting and TFP growth at the level of nations. Do nations with more patents also experience more productivity growth? The challenge here is that different countries have different standards around what constitutes a patent. To apply a uniform standard, Porter and Stern exploit the fact that many international firms seek to enter US markets, and hence obtain patents at the US patent and trademark office. So rather than use the number of patents each country has at its domestic patent office, they look at how many patents firms in different countries seek at the US patent office, so that a consistent standard is applied. They focus on 16 OECD countries from 1973-1993, and construct “patent stocks” for each country - these are essentially sums of prior patenting, weighted so that more recent patents count for more (see here for much more). They find that a 10% increase in this national patent stock is associated with 0.5% greater national TFP growth (and this result is statistically significant).

Patent Value and Productivity

One reason that simple patent counts don’t correlate very well with productivity growth could be that productivity growth is plausibly a noisier measure of innovation than the others we’ve discussed so far. Since the link between patents and the other measures of innovation is already small, it could be that with a noisier measure of innovation, the link becomes too small to discern. However, a number of papers have shown that if you reduce some of the noise in the patent data, you can identify a link between patents and TFP growth.

Kalyani (2024), discussed above, is not actually primarily concerned with whether patents are a good measure of innovation. Instead, it’s a paper about identifying which patents track genuine technological progress. Kalyani develops a new approach to try and separate the patent wheat from the chaff. Specifically, Kalyani processes the text of patents to identify technical terminology and then looks for patents that have a larger than usual share of new technical phrases (think “machine learning” or “neural network”). He dubs patents above the 90th percentile in their use of new phrases “creative” patents. About 14% of patents are creative by this definition.

While the link between raw patent counts and TFP growth cannot be statistically distinguished from zero, if you instead count Kalyani’s creative patents, you get a pretty robust correlation. Among individual firms, a 10% increase in creative patents is associated with roughly 2% higher TFP growth. At the industry level, a 10% increase in creative patents is associated with roughly a 10% increases in TFP growth. In both cases, the estimates are now statistically distinguishable from zero.

Kogan et al. (2017) also find that improved measures of patenting are correlated with TFP growth. They have data on publicly traded firms, from 1926 through 2010, including information on each firm’s patents and firm’s TFP growth. Recognizing that patents vary substantially in their value, they take two approaches towards estimating the value of patents. In one approach, the value of a patent is related to how many citations it receives. A patent that receives no citations is worth 1, a patent receiving an average number of citations (for the year it was granted) is worth 2, and a patent receiving twice the average number of citations is worth 3, for example. Their other approach looks at how the stock price of the patent-holder changes when the patent is granted - they use these movements to try and infer what the market thinks these patents are worth, at the time they are granted.

Using each of these measures, they look at how the total estimated value of a firm’s patents is correlated with the firm’s TFP growth (where a patent’s value either comes from information on citations or stock price movement). A 10% increase in the value of a firm’s patents is associated with a 0.5-1.0% increase in TFP growth (when value is based on citations received) or 1.3-2.4% in TFP growth (when value is based on stock moves). Again, in both cases, we can estimate the association with enough precision to statistically distinguish them from zero.

Summing Up

So to sum up, across a variety of indicators, we see a positive association between patenting and measures of innovation. When there are more patents, firms are more likely to offer products with new UPC codes or semiconductors with improved storage capacity. We observe a similar relationship between rates of technical improvement and the number of patents for a wide range of technologies. Finally, there is a pretty tight correlation between R&D spending and patenting.

When we look at productivity growth, the evidence is more mixed. Raw patent counts and TFP growth are not generally robustly correlated (though one paper finds this at the level of nations). But if we try to improve on raw patent counts by separating out good and bad patents, various measures of “good” patents tend to be consistently and positively associated with TFP growth.

But there’s an important caveat. As a general rule, the link is a small one - far below a 1 for 1 proportional correlation. Increase patenting by 10% and you’ll typically see much less than a 10% increase in whatever measure of innovation you’re using.

Thanks for reading! The next post in this series will be posted to Substack tomorrow - stay tuned! As always, if you want to chat about this post or innovation in generally, let’s grab a virtual coffee. Send me an email at matt.clancy@openphilanthropy.org and we’ll put something in the calendar.