Maybe There is No Technological Slowdown

Reflections on Fully Grown by Dietrich Vollrath

I just finished reading Fully Grown: Why a Stagnant Economy is a Sign of Success by Dietrich Vollrath. The book is a deep dive into economic statistics that implicitly argues there’s not much evidence for a “technological stagnation” over the last several decades.

The Slowdown

The puzzle Vollrath sets himself to explain is why GDP per capita growth in the US averaged 2.25% for the latter half of the 20th century, but only 1.00% in the first 20 years of the 21st century. This is not just due to the negative pull of the great recession. Growth was weaker before and after the recession too.

(Note that, unlike some other stagnationists, Vollrath is focused on the relatively recent growth slowdown; this isn’t a book about the difference between growth in the 50 years before and after 1970)

One explanation for this is that something has gone wrong with technological progress. There are a variety of takes on the question of technological stagnation, but one throughline is that advances in digital technology have not been enough to offset stagnating innovation in the physical world. We’re enjoying innovation in bits, not atoms - “we wanted flying cars and got 140 characters.”

The trouble with this hypothesis is that it’s hard to test. Even if you limit yourself to testing for technological slowdowns in a single industry, it can be hard to know what to measure. For instance, is stagnation in the speed of air travel evidence of an innovation deficit? Or are improvements in fuel efficiency, noise pollution, and safety evidence of an innovation surplus? Or take agriculture: do you look at crop yields? Or crop resilience? Or reductions in the use of other inputs? (I wrote a whole thread last Thanksgiving about how hard it is just to measure the impact of genetic engineering on corn).

The problem is even harder when you want to talk about “technology” writ large. How do you create an index of technology that encompasses advances in everything from airplanes to agriculture? Well, one way to go is to use economic proxies.

The most basic measure of “technology” is simply GDP per capita. All else equal, better technology leads to more economic output. But everyone knows this is imperfect, since GDP per capita can be affected by inputs - more capital, more education, etc - in addition to technology. Better to use total factor productivity (TFP), which is a measure of how much “extra” GDP you get after attempting to account for all those inputs. Since TFP represents a measure of how efficiently inputs are translated into outputs, it is frequently used as a proxy for overall technology.

Now: everyone knows that if you want to use GDP per capita or TFP as a proxy for overall technology, you have to include the caveat that “these measures are not perfect.” But then, most people go on to use them because… what else are you gonna do?

One of Vollrath’s contributions is to underscore just imperfect these measures are as proxies for technological change. Vollrath shows it can easily be the case that technological progress did not slow at all, and that the slowdown in real GDP per capita growth and TFP growth is entirely driven by non-technological factors.

What Caused the Slowdown?

Vollrath’s preferred decomposition of the causes of the 1.25% annual slowdown in real GDP per capita growth is:

0.80pp - Declining growth in human capital

0.20pp - The shift of spending from goods to services

0.15pp - Declining reallocation of workers and firms

0.10pp - Declining geographic mobility

The first striking thing about this is that changes in human capital alone accounts for two-thirds of the slowdown. The decline in the growth of human capital stems from four main factors: older workers, fewer workers, fewer hours worked, and stabilizing educational attainment. Of these the biggest shift is the decline in the number of workers per capita, which stems from the choice rich societies made to have fewer children.

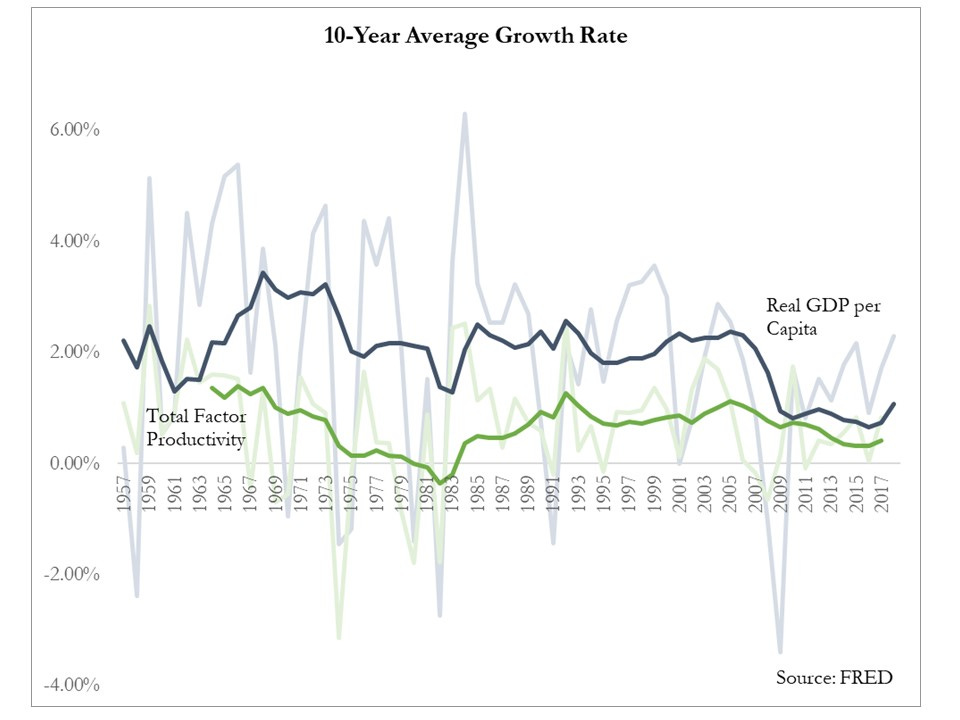

This leaves about 0.45pp left over for explanations related to the capital stock and TFP. Indeed, you can see in the graph above that GDP per capita growth drops noticeably in 2007, but TFP growth only drops a bit. Thus, right off the bat, Vollrath argues a slowdown in technological progress explains at most part of one-third of the growth slowdown.

But Vollrath goes farther and argues the drop in TFP growth likely has non-technological explanations.

Shifting Preferences

TFP growth for the entire economy is the weighted average of TFP growth across the different sectors that make up our economy. The weights are determined by spending shares across sectors: if we spend 60% our income on goods and 40% our income on services, then economy-wide TFP growth is 60% TFP growth of goods and 40% TFP growth of services. The trouble is, these shares change over time. It could be that within each sector, TFP growth has remained unchanged, but we shift our spending towards sectors with slower TFP growth. This would pull down our measure of economy-wide TFP growth, even though no sector is slowing down.

Now, that’s not exactly what happened. Various sectors have seen a slowdown in TFP growth. But it turns out a large chunk of the TFP slowdown can be accounted for by the shift in our spending from goods to services. TFP growth in goods is typically faster than for services, and so putting more weight on the TFP growth of services has lowered economy-wide TFP growth.

Why is TFP growth in services slower? Well, recall that TFP is a measure of how much extra output you can get from a given set of inputs (labor and capital). For goods, we don’t really care about what the inputs were; all we want is the output (a new TV, iPhone, coat, whatever).

But many services involve the purchase of attention from someone: childcare workers, doctors, restaurant servers, and so on. To the extent you are paying for attention from someone, it’s very hard to improve TFP. For these kind of services, TFP growth would entail finding a way to get more minutes of attention out of the same number of workers. Since we all have the same 24 hours in a day, it’s not clear where the extra attention can come from. More on this next week.

The Rest of the TFP slowdown

Human capital and the shift to services accounts for about 80% of the slowdown. The remaining 20% is driven by reduced entry and exit of firms and reduced job changes. Since more productive firms tend to supplant lower productivity ones, and since workers tend to move to higher wages (and therefore, higher productivity, if standard economics is mostly right), when firm and job turnover slows, this can reduce TFP growth.

The slowdown in entry of higher productivity firms might be one manifestation of a technological slowdown. Maybe, for instance, a reduction in cost-reducing and quality-enhancing innovations is reducing the supply of new business models? But there are also other possible causes. It might be that lax antitrust policy has led to an increase in market power. Others argue the slowdown in firm entry is another consequence of our decision to have less children back in the 1970s.

The decline in geographic mobility could also have worrying and benign causes. It may be that workers want to move to higher productivity regions, but are locked out by the rapidly rising price of housing. This, in turn, might be due to policies in major cities that restrict the housing supply. But, it could also be that people don’t actually like to move and the high rates of mobility in the late twentieth century are the real aberration.

So most of the reason for the slowdown in growth has to do with choices people made. Between preferences for smaller families, fewer work hours, and services over stuff, Vollrath argues you can account for 80% of the growth slowdown. And it’s not clear the remainder can be easily blamed on a technological slowdown.

Is this a good thing or a bad thing? Vollrath argues maybe it’s good! I’ll turn to that part of his argument next week.